Ironwood Investment Management, LLC, has long been a specialist in the small cap equity space, leveraging their expertise to identify high-quality companies with growth potential. Their focus on small cap stocks is not just a niche strategy, but a well-reasoned approach based on historical market trends and economic cycles. As we look ahead to potential economic shifts, particularly in interest rates, it’s worth examining how Ironwood’s Small Cap Core Strategy might be positioned to benefit investors.

The Small Cap Advantage in Changing Interest Rate Environments

Historically, small cap stocks have shown a tendency to outperform their large cap counterparts during periods of declining interest rates. Below, we cite a few historical examples where small caps outperform large caps in declining interest rate environments:

July 2024: In the most recent example, the discussion and increasing likelihood of an interest cut precipitated a dramatic jump in the Russell 2000 Small Cap Index, which increased 10.2% in the month of July 2024, versus 1.0% in the S&P 500, an outperformance of 9200 bps in a single month.

With the anticipation and increasing likelihood of an interest rate reduction in the medium term, the Russell 2000 outperforms the S&P 500 by 9200 bps in the month of July

Source: Yahoo Finance; date range: 7/1/2024 – 7/31/2024.

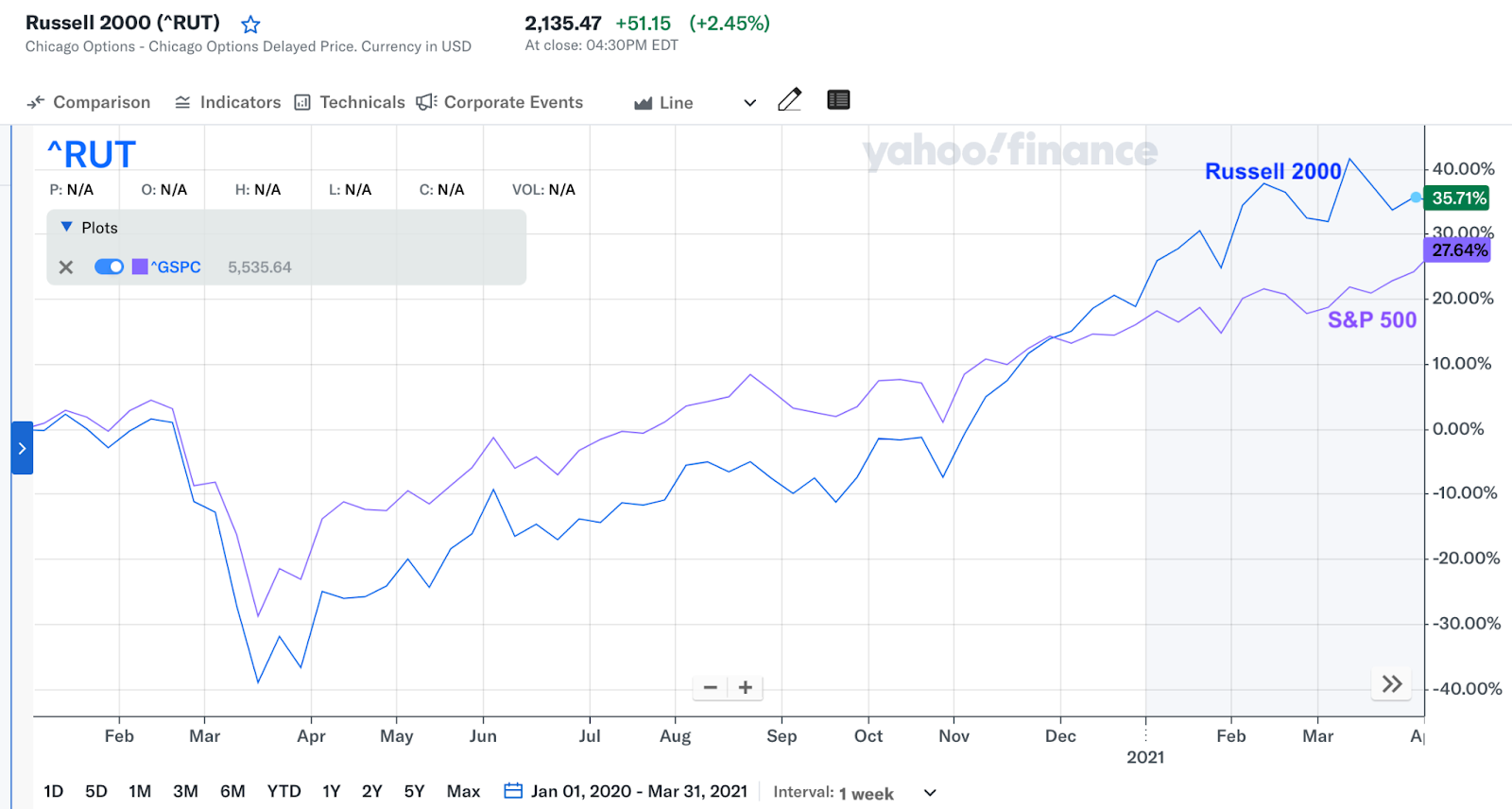

COVID Pandemic: The Fed cut rates three times in 2019 and then dramatically in early 2020 due to the COVID-19 pandemic. While the pandemic created unique circumstances, small caps showed strong relative performance in the recovery phase, particularly from late 2020 into 2021.

The Fed decreases interest rates in light of the global COVID pandemic, bringing rates down from 2.40% in July 2019 to 0.05% in May 2020. In the chart below, we see the Russell 2000 crossover and outperform the S&P 500 in approximately Dec 2020.

Source: Yahoo Finance; Federal Reserve Bank of St. Louis, Fred Economic Data; date range: 1/1/2020 – 3/31/2021.

2008-2009 Global Financial Crisis: As the Fed slashed interest rates to near zero in response to the financial crisis, small caps again showed strong relative performance once the market began to recover in 2009. The Russell 2000 rebounded more quickly than the S&P 500 in the initial stages of the recovery.

During the Global Financial Crisis, the Fed reduces rates from 5.26% in July 2007 down to 0.15% in January 2009. We see the Russell 2000 cross over the S&P 500 in approximately March 2009, after the massive rate cut has taken effect. The Russell 2000 index outperforms the S&P 500 in the remainder of the time period shown below.

Source: Yahoo Finance; Federal Reserve Bank of St. Louis, Fred Economic Data; date range: 1/1/2008 – 12/31/2010.

2001-2003 Post-Dot Com Bubble: Following the dot-com bubble burst, the Federal Reserve began cutting interest rates aggressively. During this period, small caps significantly out-performed large caps. The Russell 2000 (small cap index) outperformed the S&P 500 (large cap index) by a wide margin.

In the post-dot com bubble era, the Fed Funds rate drops from 6.40% in December 2000, to 1.72% in January 2002. We see the Russell 2000 index begin to outperform the S&P 500 in approximately May 2000, and continue to outperform the S&P for the duration of the period shown in the chart below.

Source: Yahoo Finance, Federal Reserve Bank of St. Louis, Fred Economic Data; date range: 1/1/2000 – 12/31/2002.

These examples illustrate the historical tendency for small caps to outperform in declining rate environments; it’s important to note that each economic cycle has its unique characteristics, and past performance doesn’t guarantee future results. Additionally, other factors beyond interest rates can significantly influence relative performance between small and large caps.

The Ironwood Advantage: A Quarter Century of Small Cap Investing

For over 25 years, Ironwood Investment Management, LLC has had a disciplined approach in small cap equity investing. Ironwood’s flagship Small Cap Core strategy, launched in 1999, has built a track record through multiple market cycles: since inception (1/1/1999), the strategy has returned approximately 12% gross of fees in average annual returns, over 378 bps in alpha versus the Russell 2000 benchmark index.

Ironwood’s investment philosophy and process are well-suited to navigating this potentially opportune environment for small caps. The focus on identifying high Ironwood-Quality (“High I-Q”) companies positions them to select small cap stocks that not only might benefit from a short-term rate-driven rally but also have the fundamental strength to deliver long-term value.

Learn more about Ironwood and the firm’s track record of success.

Conclusion: Market Dynamics May Present A Timely Opportunity

As we approach a potential September rate cut, Ironwood’s focus on small cap stocks seems particularly well-timed. For investors intrigued by this potential opportunity, engaging with experienced small cap managers like Ironwood may provide a balanced way to gain exposure to this dynamic segment of the market. The expertise in navigating the complexities of small cap investing, combined with a potentially favorable macro environment, may present an interesting proposition for investors looking to position their portfolios for both immediate opportunities and long-term growth.

PERFORMANCE DATA AND DISCLOSURES

Performance Statistics as of 6/30/2024

Ironwood Investment Management®, LLC (Ironwood) is an independently managed investment advisory firm providing investment advisory services to institutional clients, mutual funds and high-net-worth clients. The firm is a registered investment adviser with the Securities and Exchange Commission. SEC Registration does not imply a certain level of skill or training. Accounts in the Small Cap Core composite include separately managed, fully discretionary, fee-paying portfolios. Portfolios are invested in undervalued securities, the majority of which will have market capitalizations under $2.5 billion at cost, including securities with growth and/or value characteristics. Securities are considered undervalued when management believes the current share price does not accurately reflect the long-term economic value of the underlying company. Ironwood Investment Management, LLC claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Ironwood Investment Management, LLC has been independently verified for the periods January 1, 1999 through December 31, 2021. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The Small Cap Core composite has had a performance examination for the periods July 1, 2002 to December 31, 2021. The verification and performance examination reports are available upon request. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. The creation date of the composite: July 2002. Performance inception date of the composite: January 1, 1999. Prior to July 2002, portfolios were included in the composite when at least 75% of the portfolio was invested in equity securities and when at least 75% of the portfolio was invested according to the investment style of the composite. Subsequent to July, 2002, portfolios are included in the composite after the first full month of being fully invested. Returns are presented gross and net of management fees and include the reinvestment of all income. Net returns are calculated based on the highest fee of 1.00%. Investment management fees are 1.00% on the first $25 million, 0.90% on the next $25 million, 0.80% on the next $50 million, and 0.75% over $100 million on an annual basis and a client’s return will be reduced by these and other related expenses. The actual fee charged to an individual portfolio may vary by size and type of portfolio and may be negotiated. Actual investment advisory fees incurred by clients may vary. The Russell 2000 Index consists of the 2000 smallest stocks in the Russell 3000 Index that represents approximately 8% of the U.S. equity market capitalization. The indices have been reconstituted annually since 1989. Ironwood returns and Index performance reflect reinvested interest income and dividends, in U.S. dollars. A list of composite descriptions and a list of limited distribution pooled fund descriptions are available upon request. Past performance is not indicative of future results. Policies for valuing investments, calculating performance and preparing GIPS Reports are available upon request. Prior to May 2006, the Firm was known as Ironwood Capital Management, LLC.